Types of Cheques

Types of Cheques

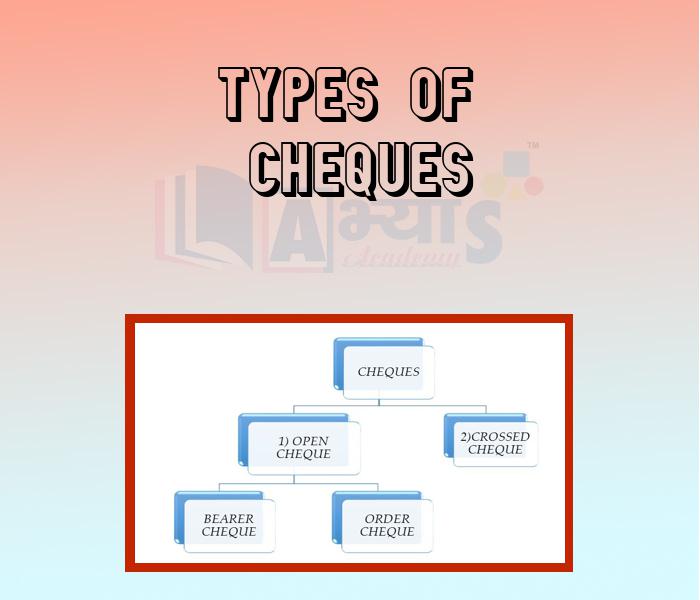

Types of Cheques :

Types of Crossing:

(a) General Crossing : In a general crossing, simply two parallel transerve lines, with or without the words the words not negotiable in between, may be drawn. Such a cheque is crossed generally. The effect of general crossing is that the payment of the cheque will not be made at the counter; it can be collected only through a banker.

(b) Special Crossing: In a special crossing, the name of a banker with or without the words not negotiable is written on the cheque. Such a cheque is crossed specially to that banker .The effect to special crossing is that the paying banker will transfer the amount of the cheque only through the bank named in the cheque.It should be noted that two transverse parallel lines are necessary for a general crossing, whereas for a special crossing, no such lines are necessary.

(c) Restrictive Crossing: This type of crossing has been recognised by usage and custom the trade. In a restrictive crossing, the words 'Account Payee' or 'Account Payee Only are added to the general or special crossing The effect of restrictive crossing is that the payment of the cheque will be made by the bank to the collecting banker only for the account payee named. If the collecting banker collects the amount for any other person, he will be liable for wrongful conversion of funds.

(d) Not Negotiable Crossing: A cheque crossed generally or specially, bearing in either the words 'not negotiable' shall not be able to give a better title to the holder than that of the transferor. The effect of a not negotiable crossing is that the cheque can be transferred but the transferred will not acquire a better title to the cheque. Thus, a cheque is deprived of its essential features of negotiability. The object of "not negotiable" crossing is to protect the drawer against loss or theft in the course of transit.

5. Ante-Dated Cheque: If a cheque bears a date earlier than the date on which it is presented to the bank, it is called as "anti-dated cheque". Such a cheque is valid upto three months from the date of the cheque.

6. Post-Dated Cheque: If a cheque bears a date which is yet to come (future date), then it is known as post dated cheque. A post dated cheque cannot be honoured earlier than the date on the cheque

7. Stale Cheque: If a cheque is presented for payment after three months from the date of the cheque, it is called stale cheque. A stale cheque is not honoured by the bank.

Account Payee Cheques can be paid _________________ | |||

| Right Option : C | |||

| View Explanation | |||

Students / Parents Reviews [20]

When I have not joined Abhyas Academy, my skills of solving maths problems were not clear. But, after joining it, my skills have been developed and my concepts of science and SST are very well. I also came to know about other subjects such as vedic maths and reasoning.

Sharandeep Singh

7thMy experience with Abhyas is very good. I have learnt many things here like vedic maths and reasoning also. Teachers here first take our doubts and then there are assignments to verify our weak points.

Shivam Rana

7thIt has a great methodology. Students here can get analysis to their test quickly.We can learn easily through PPTs and the testing methods are good. We know that where we have to practice

Barkha Arora

10thA marvelous experience with Abhyas. I am glad to share that my ward has achieved more than enough at the Ambala ABHYAS centre. Years have passed on and more and more he has gained. May the centre flourish and develop day by day by the grace of God.

Archit Segal

7thOne of the best institutes to develope a child interest in studies.Provides SST and English knowledge also unlike other institutes. Teachers are co operative and friendly online tests andPPT develope practical knowledge also.

Aman Kumar Shrivastava

10thThird consective year,my ward is in Abhyas with nice experience of admin and transport support.Educational standard of the institute recumbent at satisfactory level. One thing would live to bring in notice that last year study books was distributed after half of the session was over,though study ...

Ayan Ghosh

8thAbout Abhyas metholodology the teachers are very nice and hardworking toward students.The Centre Head Mrs Anu Sethi is also a brilliant teacher.Abhyas has taught me how to overcome problems and has always taken my doubts and suppoeted me.

Shreya Shrivastava

8thIn terms of methodology I want to say that institute provides expert guidence and results oriented monitering supplements by requsite study material along with regular tests which help the students to improve their education skills.The techniques of providing education helps the students to asses...

Aman Kumar Shrivastava

10thAbhyas is good institution and a innovative institute also. It is a good platform of beginners.Due to Abhyas,he has got knoweledge about reasoning and confidence.My son has improved his vocabulary because of Abhyas.Teacher have very friendly atmosphere also.

Manish Kumar

10thAbhyas institute is one of the best coaching institute in the vicinity of Ambala cantt.The institute provides good and quality education to the students.The teachers are well experienced and are very helpful in solving the problems. The major advantages of the institute is extra classes for weak...

Shreya Shrivastava

8thAbhyas is a complete education Institute. Here extreme care is taken by teacher with the help of regular exam. Extra classes also conducted by the institute, if the student is weak.

Om Umang

10thWe started with lot of hope that Abhyas will help in better understnding of complex topics of highers classes. we are not disappointed with the progress our child has made after attending Abhyas. Though need to mention that we expected a lot more. On a scale of 1-10, we would give may be 7.

Manya

8thMy experience with Abhyas academy is very good. I did not think that my every subject coming here will be so strong. The main thing is that the online tests had made me learn here more things.

Hiya Gupta

8thIt was a good experience with Abhyas Academy. I even faced problems in starting but slowly and steadily overcomed. Especially reasoning classes helped me a lot.

Cheshta

10thAbhyas is an institute of high repute. Yogansh has taken admission last year. It creates abilities in child to prepare for competitive exams. Students are motivated by living prizes on basis of performance in Abhyas exams. He is satisfied with institute.

Yogansh Nyasi

7thBeing a parent, I saw my daughter improvement in her studies by seeing a good result in all day to day compititive exam TMO, NSO, IEO etc and as well as studies. I have got a fruitful result from my daughter.

Prisha Gupta

8thMy experience with Abhyas academy is very nice or it can be said wonderful. I have been studying here from seven class. I have been completing my journey of three years. I am tinking that I should join Abhyas Academy in tenth class as I am seeing much improvement in Maths and English

Hridey Preet

9thIt was good as the experience because as we had come here we had been improved in a such envirnment created here.Extra is taught which is beneficial for future.

Eshan Arora

8thUsually we see institutes offering objective based learning which usually causes a lag behind in subjective examinations which is the pattern followed by schools. I think it is really a work of planning to make us students grab the advantages of modes of examination, Objective Subjective and Onli...

Anika Saxena

8thThe experience was nice. I studied here for three years and saw a tremendous change in myself. I started liking subjects like English and SST which earlier I ran from. Extra knowledge gave me confidence to overcome competitive exams. One of the best institutes for secondary education.